An event in the making since 2007

This is kind of a special moment for me. Since the year 2007, which is eight years ago or 20 percent of my time alive on this Earth, I have been stuck with a less-than-ideal real estate situation. And it is just about to be resolved with the happy CHA-CHING! of a cash register.

To make

the long story short, my old house building company created a fancy, modern house just in time for the late-2000s housing crash. After two years of listing it for sale and dropping the price, I took it off the market. Instead of selling it into the void at 50% off, I put it on the backburner as a rental house. Since then, it has generated generous monthly checks in exchange for a low level of background stress in my life.

Finally, our local real estate market has recovered fully and the time has come to put this place on the market, and so that is where our story begins today.

And it’s not just my story – selling a house is a big deal for many people. It can be a stressful event, or a looming unknown for those who have never done it before. This fear keeps people stuck in one place while

commuting to another, or locked up on top of a million dollars of equity, when they could easily use that money to retire young and live somewhere else.

Loosening up your feelings about selling a house can provide a surprisingly big life boost. As a side benefit, knowing how to do it well will add money to your life while subtracting stress.

With my habit of renovating houses and moving around a little plus a wife who is a licensed real estate agent, I’ve been through a few more house transactions than average. But my Honey Badger tendencies have gotten me stung plenty of times, so I have seen the cruel side of the real estate market just as much as the generous. Because of this history, I figured it would be worth peeking in on my current house-selling adventures as an example.

What Selling Means

At the core, when you sell something you are becoming a salesperson. This means finding out who your customers are and what they want, then figuring out how to make your product appeal to them. You can pretend this is not true, and in a hot enough market you may even get away with it, but in general you tend to get walked over if you ignore the realities of your customers.

Knowing Your Customer

When I bought and renovated my first house at age 25, I saw things only through my own narrow lens. I was an engineer, so of course I assumed that advanced network wiring to every room would be valuable to everyone. I was young and fit and had no children, so of course we didn’t need three bedrooms on the main floor, or guardrails to protect the basement staircase.

Eventually, I applied this self-centered vision to my housebuilding company in 2005 and built something the market did not value as much as I had hoped. I liked modern, open houses which worship the Sun. Big windows. Exposed structural beams. Welded steel. Stone tile that goes all the way to the ceiling. While I shared this housing taste with Dwell Magazine and Los Angeles thirtysomethings, it turned out that my customers at the time were non-coastal people two decades older than me, looking for traditional Victorian-themed homes with enough bedrooms for their kids. They didn’t care at all about how many square feet of South-facing glass a house contained.

Similarly, if you’ve lived in your house for a long time and are getting ready to sell it, you might find that the people moving into your neighborhood are a different crowd than those moving out. Blue carpet and flowery country-style wallpaper were homey touches in 1982, but have become quite destructive to resale value here in 2015.

The bottom line is that your house will sell better if it matches the desires of your ideal customer. A full decade later, people my age (who I find more likely to have similar tastes) can finally afford houses like the ones I built, which means the local market finally likes the same things I do. At last, we pass the Customer Test.

Becoming One With Your Local Housing Market

Almost ten years ago, I signed up for an automated email system that alerts me of every house listing and every sale that takes place in my neighborhood. Although I would not recommend this for people not interested in real estate, it has been fascinating to me. Over time, you develop a deep intution for spotting deals and ripoffs at the moment of listing, which you can refine by watching how quickly or slowly each house sells. Then when it comes time to sell your own house, you know exactly how to price it to hit the fine line of maximum profit.

In the case of the rental house I’m selling right now, similar homes were selling in the $550k-$600k range, so I set my price at $565,000.

Preparation for Sale

House buyers are in an amazing situation: they are making a spectacularly expensive purchase after only 30-60 minutes of touring the product. This means that they operate based on first impressions and rapid evaluation of the spaces. And thus your house needs to hold up well to this type of evaluation. It’s worth reading a whole book on this, but to summarize quickly:

- Think Open and Airy: When buyers walk in, they need to be confronted with light, space, and charm. So eliminate anything that blocks this feeling – open the curtains, clean the windows, and remove stuff like baby gates or pet crates.

- Renovations: In higher-end markets, strategic renovations including a modern kitchen, knocking out unnecessary interior walls, and (oddly enough) a great front door will return more than 100% of the cost in eventual resale. The key is in watching that cost: even hiring out all the work, a new kitchen with good cabinets, stone countertops and quality fixtures should total under $25,000 rather than the $75,000 many people end up forking over.

- Stage the House: If it’s empty, hire a staging company. If you still live there, remove most of your stuff and have only sparse, tasteful decor. Selected artwork, a nice table arrangement with flowers, the perfect books on the shelves, and so on. Buyers will claim that they can look past a mess, but it just isn’t true. The well-staged houses get statistically higher and faster offers, which makes it a profitable choice – especially in higher priced markets. I spent about $1600 to hire Design Matters Home, which covered design plus all the furniture rental and moving.

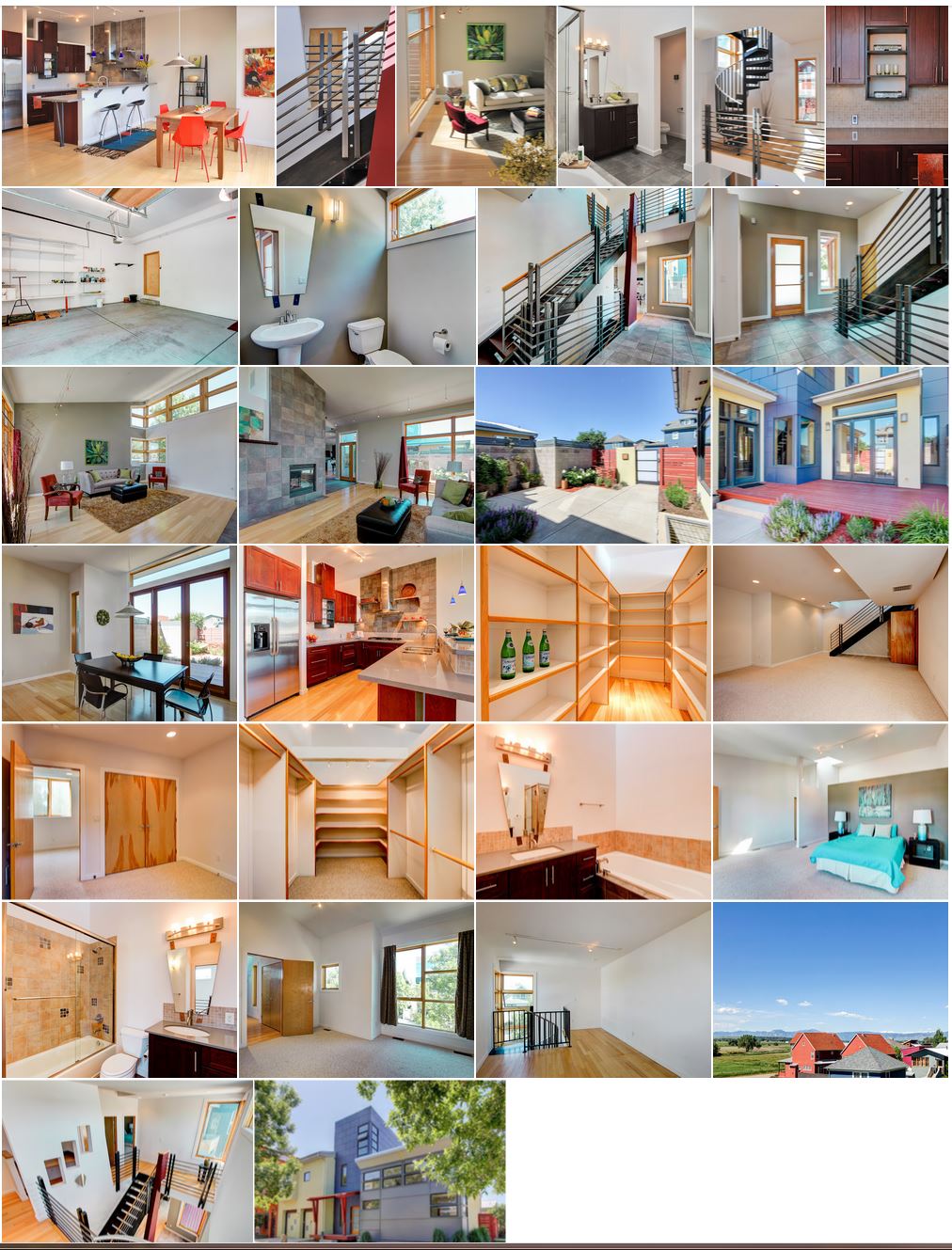

- Photography: this is critical, cheap, and yet usually overlooked. How many real estate listings feature blurry, dim pictures of the corners of rooms taken by the listing agent running around with an iPhone for a few minutes? To do it right, you need an SLR camera with a tripod and roughly a 10-22mm wide angle lens. Or hire an affordable pro – I was able to get a great real estate photographerto shoot my house, plus process and deliver about 50 digital images for under $100. Money well spent (and thanks Josh!)

Let’s compare the effect of lackuster versus professional photography with a real-world example.

Figure 1: These are the actual pictures from a recent $425,000 listing in my area. Four hastily-taken pictures. Seriously?

Figure 2: Since the system allows up to 25 pictures, I provided 25. Each with a full text description (most real estate agents leave the description field blank).

Hire an Agent or Sell it Yourself?

Even Mrs. Money Mustache (an accredited agent herself) admits that there is no special difficultly involved in what real estate agents do. While there are surely some brilliant, talented and hardworking people in the field, the hard truth is that only a minority of the agents either of us have met would fit this description. Besides, the real work is making the product great and getting it in front of buyers. In the US, this means getting your property listed in the MLS (multiple listings system). Although it is an antiquated and proprietary system, it is still where most buyers are shopping so you need to be in it to win it.

Suggestion: hire an intelligent and dynamic agent if you can find one and are not interested in doing the work yourself. Otherwise, hire a discount fee-for-services agent, or just put your place on Craigslist and then pay separately to get it into the MLS.

Most of your buyers, unfortunately, will still be shopping with a buyer’s agent, so you should expect to fork over 2.8% of your purchase price to pay his or her fee if you want access to that big pool of shoppers.

Showings, Offers and Negotiation:

Once you get the place listed, you are off to the races. Buyers will find it on the MLS system as well as Craigslist if you listed it there. They book appointments, review your hard work, and if you are lucky, make you an offer.

There will be negotiations, an inspection, and various deadlines and hurdles to clear, and the level of stress all depends on what type of market you are in: in a slow market, buyers might ask you to replace the whole furnace or roof, and walk away to the next deal if you don’t comply. In a fast one, you can safely reject anything silly and the buyers will tend to give in, lest they lose yet another house to other competitive buyers.

Pro Tip: Normally, buyers can make an offer at any time and you have 24 hours to respond. But if you write something like “All offers will be reviewed on Saturday July 11th at 12PM”, you can wait a week or so to collect multiple offers and respond to everyone at once. This increases your chance at having multiple options and creates competition between buyers, which increases your leverage in negotiations.

So Should you Do it?

Selling your house is always going to take some work, no matter how you approach it. But if you do the math right, it can be some of the highest paid work around, and come with great lessons in human nature as well. I have never regretted a sale and have many good memories (and dollars) to show for the hard work of the past.

At the same time, you should think about the work of eventually selling any house before buying it in the first place. If you’re not ready to devote a few weeks at some point in the future, and potentially absorb a 20% loss if you need to move in a down market, you should definitely consider renting instead.

Epilogue:

I started writing this article a few weeks ago, as Mrs. MM and I were working through all of these steps ourselves. We were ready at last on June 9th, finishing the last details and getting everything uploaded into the system just before midnight.

Just after breakfast the next morning, the phone rang with an incoming number from a Hawaiian area code. Some new arrivals to Longmont had studied our listing in detail and were very excited to tour the house in person. We agreed on an appointment time of high noon on that same day.

I biked down to the house to meet the prospective buyers, and we immediately got along like old friends. The house tour was more of a celebration of our shared tastes in home design, and they were full of questions about how every detail had been designed and built.

Before leaving, they gave me a verbal, full-price offer with no buyer’s agent to suck money out from the middle of the deal. In other words, $565,000 with no funny business, heading directly to our investment account in just a few weeks. We shook hands and I thanked them for their wonderful interest and the offer.

Following the Pro Tip above, we left the place on the market for a full week, collecting two more solid offers – but nothing quite as good as that first offer, because cutting out a buyer’s agent made their offer effectively 2.8% higher (about $16,000). So we sealed the deal, the house is under contract, closing will be next month, and all is well.

SOLD!!!

I wish you even better luck than I’ve had in your own real estate adventures. Own the house you truly want to own, sell any that don’t fit that description, and prosper.