Many people earning a standard salary think their net worth is only defined by their savings. However, I want to let you know that you are very rich! In today's loose monetary policy, where the cost of borrowing is less than the cost of inflation, why would you want to wait and save the money...?

This period is hard to come by, in today's economic condition is favourable to borrow and invest. The returns on investment is often more than the cost of borrowing. Today if you earn $5000 a month, your net worth potential is 4x$5000 per bank! If you have good relationship with 10 banks... your net worth is $200,000.

Now where is the risk limit?

Each bank can give you an unsecured loan at about 6% today for up to 4 x your monthly salary.

The repayment, interest plus principal is about $500 a month per loan for up to 5 years.

Say you have $3000 cashflow per month.

You potentially can leverage 6 x $20,000 - $120,000 at a cost of $3000 a month. Use this money to invest in an asset that gives you at least 8% rental yields per annum. You can have a forced savings plan in place. People talked about leaving an asset for their family, instead of insurance policy, why not consider property? You can apply for a insurance that covers your loan in case anything happens.

A good asset is property. As we know property cycle, property price doubles every 7 years, in 5 years time, we conservatively estimate the previous property gained 20% at 4% per annum. You could earn 2% yields * 5 years = 10% plus 20% capital gains. A total of 30% yields.

Learn to use bank loans to help you achieve your investment goals.

Tuesday 23 April 2013

Phillipines - the Emerging Star in Real Estate

When we look into areas to invest, I always start at the Macro Level, Strong GDP growth and strong demographics. The outlook for Phillipines is great and it has one of the highest population growth rates in Asia at 2.04% according to a 2010 census and its population is set to grow even further in the coming years due to improved economics and healthcare. According to a research report, the population of phillipines may reach 101.2 million by 2014.

Phillipines' main city is Manila and it is an urban metropolis and is ever expanding due to rural, urban migration and a strong economy. It is a MEGAPOLIS.

As an investor, I am concerned about the working population and the educational level. The rate of urbanisation is great at 2.3% and the main bulk of the population is 25-54 which is 36% of the population. This is a fantastic demographics. 36% of the workforce is at a productive age and the next wave in the next 30 years, the 0-14 age group is at 34.3%. It just screams " We need housing " to you!

Looking at the GDP Growth rate of 6.2% shows that its economy is strong and the wages should be rising as well. Phillipines is indeed a rising star in Real Estate.

Before you embark on any investment, it is always wise to conduct your own research into the laws and management. A property without management is not going to work.

Here are some facts for you to digest :

rate of urbanization: 2.3% annual rate of change (2010-15 est.)

The following Websites for more information.

http://en.wikipedia.org/wiki/Demographics_of_the_Philippines

http://www.indexmundi.com/philippines/demographics_profile.html

https://www.google.com.sg/publicdata/explore?ds=d5bncppjof8f9_&met_y=ny_gdp_mktp_kd_zg&idim=country:PHL&dl=en&hl=en&q=philippines%20gdp%20growth

Phillipines' main city is Manila and it is an urban metropolis and is ever expanding due to rural, urban migration and a strong economy. It is a MEGAPOLIS.

As an investor, I am concerned about the working population and the educational level. The rate of urbanisation is great at 2.3% and the main bulk of the population is 25-54 which is 36% of the population. This is a fantastic demographics. 36% of the workforce is at a productive age and the next wave in the next 30 years, the 0-14 age group is at 34.3%. It just screams " We need housing " to you!

If Manila grows at 2% a year - it will require about 69,000 new housing a year at 3.9 pax per household. If Manila's population is mostly yuppies, we can even estimate to be 138,000 new housing a year. Thats a lot!

Looking at the GDP Growth rate of 6.2% shows that its economy is strong and the wages should be rising as well. Phillipines is indeed a rising star in Real Estate.

Before you embark on any investment, it is always wise to conduct your own research into the laws and management. A property without management is not going to work.

Here are some facts for you to digest :

Age structure

0-14 years: 34.3% (male 18,175,763/female 17,452,488)

15-24 years: 19.1% (male 10,107,717/female 9,753,268)

25-54 years: 36.6% (male 19,065,843/female 18,941,091)

55-64 years: 5.6% (male 2,663,592/female 3,102,247)

65 years and over: 4.3% (male 1,948,152/female 2,564,841) (2012 est.)

15-24 years: 19.1% (male 10,107,717/female 9,753,268)

25-54 years: 36.6% (male 19,065,843/female 18,941,091)

55-64 years: 5.6% (male 2,663,592/female 3,102,247)

65 years and over: 4.3% (male 1,948,152/female 2,564,841) (2012 est.)

Urbanization

urban population: 49% of total population (2010)rate of urbanization: 2.3% annual rate of change (2010-15 est.)

Major cities - population

MANILA (capital) 11.449 million; Davao 1.48 million; Cebu City 845,000; Zamboanga 827,000 (2009)The following Websites for more information.

http://en.wikipedia.org/wiki/Demographics_of_the_Philippines

http://www.indexmundi.com/philippines/demographics_profile.html

https://www.google.com.sg/publicdata/explore?ds=d5bncppjof8f9_&met_y=ny_gdp_mktp_kd_zg&idim=country:PHL&dl=en&hl=en&q=philippines%20gdp%20growth

Monday 22 April 2013

The Greater Fool Theory

The greater fool theory posits that rational people will buy into valuations that they don’t necessarily believe, as long as they believe there is someone else more foolish who will buy it for an even higher value. The human tendencies described above lead to a fairly predictable outcome: After an innovation is introduced and a market is formed, people believe both that they are among the few who have spotted the trend early, and that they will be smart enough to pull out at the right time.

Iskandar Malaysia - why it remains a dream

Iskandar, the newest Hottest Hotspot in Johor, Malaysia. Notice the duplication of Hot Hot in the previous sentence? Iskandar is Hot. Is there a reason for its hotness?

There are many pros relating to property investments in Iskandar, one of it being the cheap and abundant land. A higher standard of living brought about by new infrastructure and amenities. A few of the key initiatives for increasing demographics.

Themeparks - 2 completed, more to come.

Waterfront living - Danga Bay, Puteri Harbour, Tanjong Puteri, The Cove

1/2 priced Resort style living - Horizon Hill, East Ledang

Incentives laced business district - Medini

Wellness and Hospitality - Columbia Hospital, Raffles Hospital

Education - Maborough, Raffles, Newcastle, Dutch Maritime University

Nightlife - Mall of medini?

Recreation - Golf

Security - ?

Communityness - A Singapore based expatriat community (JSCA)

Jobs? - ?

Commercial? - ?

Transport - High Speed Rail, Ferry, MRT

There has a lot of good development coming in the next few years. How is it shaping out? I am not sure, but I'm pretty sure it is better than cyberjaya and putrajaya at this point of time.

Government's policy matters a lot and the Johor Govt has been encouraging to say the least.

Mass Crossborder Transport wise, don't even bank on it. Singapore is not going to sacrifice security for convenience. Those residents staying in HH and JB hoping to see the train crossing into Singapore, can forget about it. It means the immigration clearance and security have to step up by 3 x. Watch out for recruitment for Immigration officers. When that happens, it might.

Internal MRT? Its not going to make money for Johor. Johor is not China, it would not build a mega infrastructure for show of face. Face it (pun not intended), it is economics driving the development, why will any Johorians or expats give up driving for MRT when the cost of vehicle is so cheap?

Business wise, what brings Singapore competitive advantage in petrol refinery is not going to happen in Iskandar. JI was specially designed to meet this demand for integrated services of refinery, storage, development of by products, transport out etc seamlessly. Is that going to happen in Iskandar?

An International Finance Centre, what makes an international finance centre? Would the likes of New York, London, Tokyo, Shanghai be found in Iskandar? I beg to differ.

I believe compared to Singapore, Iskandar might be a good place to live, work and play, however, there is a critical mass and critical price point where such luxury is no longer attractive. Luckily, we are not there yet.

There are many pros relating to property investments in Iskandar, one of it being the cheap and abundant land. A higher standard of living brought about by new infrastructure and amenities. A few of the key initiatives for increasing demographics.

Themeparks - 2 completed, more to come.

Waterfront living - Danga Bay, Puteri Harbour, Tanjong Puteri, The Cove

1/2 priced Resort style living - Horizon Hill, East Ledang

Incentives laced business district - Medini

Wellness and Hospitality - Columbia Hospital, Raffles Hospital

Education - Maborough, Raffles, Newcastle, Dutch Maritime University

Nightlife - Mall of medini?

Recreation - Golf

Security - ?

Communityness - A Singapore based expatriat community (JSCA)

Jobs? - ?

Commercial? - ?

Transport - High Speed Rail, Ferry, MRT

There has a lot of good development coming in the next few years. How is it shaping out? I am not sure, but I'm pretty sure it is better than cyberjaya and putrajaya at this point of time.

Government's policy matters a lot and the Johor Govt has been encouraging to say the least.

Mass Crossborder Transport wise, don't even bank on it. Singapore is not going to sacrifice security for convenience. Those residents staying in HH and JB hoping to see the train crossing into Singapore, can forget about it. It means the immigration clearance and security have to step up by 3 x. Watch out for recruitment for Immigration officers. When that happens, it might.

Internal MRT? Its not going to make money for Johor. Johor is not China, it would not build a mega infrastructure for show of face. Face it (pun not intended), it is economics driving the development, why will any Johorians or expats give up driving for MRT when the cost of vehicle is so cheap?

Business wise, what brings Singapore competitive advantage in petrol refinery is not going to happen in Iskandar. JI was specially designed to meet this demand for integrated services of refinery, storage, development of by products, transport out etc seamlessly. Is that going to happen in Iskandar?

An International Finance Centre, what makes an international finance centre? Would the likes of New York, London, Tokyo, Shanghai be found in Iskandar? I beg to differ.

I believe compared to Singapore, Iskandar might be a good place to live, work and play, however, there is a critical mass and critical price point where such luxury is no longer attractive. Luckily, we are not there yet.

Bubbles - How are they formed?

Rule no. 1 - Never Lose Money

Rule no. 2 - Follow rule no. 1

The person who taught us this is the World's no. 1 value investor. By knowing values, we can prevent ourselves from being caught up bursting bubbles...

In today's hyper loose monetary policy, where US Dollars has devalued by 30% - does it mean the world's money increased by 30%, does it mean through bank's levarage means... this does mean world currency value has increased by 10 x? think about it? Where is the right value for assets today?

Editor’s note: Adam Nash is the chief operating officer of Wealthfront, a SEC-registered, software-based financial advisor located in Palo Alto. He was formerly executive-in-residence with Greylock Partners and VP of product management at LinkedIn. Follow him on his blog and on Twitter at@AdamNash.

Editor’s note: Adam Nash is the chief operating officer of Wealthfront, a SEC-registered, software-based financial advisor located in Palo Alto. He was formerly executive-in-residence with Greylock Partners and VP of product management at LinkedIn. Follow him on his blog and on Twitter at@AdamNash.

Rule no. 2 - Follow rule no. 1

The person who taught us this is the World's no. 1 value investor. By knowing values, we can prevent ourselves from being caught up bursting bubbles...

In today's hyper loose monetary policy, where US Dollars has devalued by 30% - does it mean the world's money increased by 30%, does it mean through bank's levarage means... this does mean world currency value has increased by 10 x? think about it? Where is the right value for assets today?

Adapted from http://techcrunch.com/2013/04/20/what-can-behavioral-finance-can-teach-us-about-bubbles/

Behavioral Finance Explains Bubbles

Editor’s note: Adam Nash is the chief operating officer of Wealthfront, a SEC-registered, software-based financial advisor located in Palo Alto. He was formerly executive-in-residence with Greylock Partners and VP of product management at LinkedIn. Follow him on his blog and on Twitter at@AdamNash.

“Bubbles are beautiful, fun and fascinating, but do you know what they are and how they work? Here’s a look at the science behind bubbles.” – About.com Chemistry, “Bubble Science”

“Double, double toil and trouble

Fire burn, and cauldron bubble.” – Macbeth, Act 4, Scene 1

Fire burn, and cauldron bubble.” – Macbeth, Act 4, Scene 1

Given the incredible volatility we’ve seen lately in the Bitcoin and gold markets, there has been a resurgence in discussion about bubbles. This topic is always top of mind in Silicon Valley, especially given that the two favorite local topics of conversation are technology companies and housing.

Defining a market bubble is actually a bit trickier than it might first appear. After all, what differentiates the inevitable booms and busts involved in almost any business and industry from a “bubble”?

The most common definition of a speculative or market bubble is when a broad-based, surging euphoria or wave of optimism carries asset prices well beyond supportable value. The canonical bubble was the tulip mania of the 1630s, but it extends across history and countries all the way up to the Internet bubble of the late 1990s and the housing bubbles in the past decade.

WHAT DO BUBBLES LOOK LIKE?

Not surprisingly, there are a number of great frameworks for thinking about this problem.

In 2011, Steve Blank and Ben Horowitz debated in The Economist whether or not technology was in a new bubble. In those posts, Steve cited the research of Jean-Paul Rodrigue denoting four phases of a bubble: stealth, awareness, mania and blow-off.

(Source: Wikipedia)

HOW DO BUBBLES HAPPEN?

In 2000, Edward Chancellor published an excellent history and analysis of market bubbles over four centuries and a wide variety of countries called “Devil Take the Hindmost: A History of Financial Speculation.” In his book, he finds at least two consistent ingredients.

Uncertainty. In almost every bubble, there seems to be some form of innovation or insight that forces people to rapidly debate the creation of new economic value. (Yes, even tulip bulbs were once an innovation, and the product was incredibly unpredictable.) This uncertainty is typically compounded by some form of lottery effect, exacerbating early pay-offs for the first actors. Think back to stories about buying a condo in Las Vegas and flipping it in months for amazing gains. This creates the inevitable upside/downside imbalance that Henry Blodget recently framed as: “If you lose your bet, you lose 100%. If you win your bet, you make 1000%.” Inevitably, this innovation always leads to a shockingly large assessment of how much value could be created by this market.

Leverage/Liquidity. In every bubble, there is some form of financial innovation that broadly increases both leverage and liquidity. This is critical, because the expansion of leverage not only provides massive liquidity to fund the expansion of the bubble, but the leverage also sets up the covenants that inevitably unwind when the bubble turns aggressively to the downside. In some ways, it’s also inevitable. When a large number of people believe they’ve found a sure thing, logic dictates they should borrow cheap money to maximize their returns. In fact, the belief it may be a bubble can make them even greedier to lever up their investment so they can “cash out” the most before the inevitable break.

BEHAVIORAL FINANCE LESSONS IN BUBBLES

Bubbles clearly have an emotional component, and to paraphrase Dan Ariely, humans may be irrational, but they are predictably irrational.

There are five obvious attributes of components of bubble psychology that play into market manias:

- Anchoring. We hear a number, and when asked a value-based question, even unrelated to the number, they gravitate to the value that was suggested. We hear gold at $1,500, and immediately in the aggregate we start thinking that $1,000 is cheap and $2,000 might be expensive.

- Hindsight Bias. We overestimate our ability to predict the future based on the recent past. We tend to over-emphasize recent performance in our thinking. We see a short-term trend in Bitcoin, and we extend that forward in the future with higher confidence than the data would mathematically support.

- Confirmation Bias. We selectively seek information that supports existing theories, and we ignore/dispute information that disproves those theories. (This also tends to explain most political issue blogs and comment threads.)

- Herd Behavior. We are biologically wired to mimic the actions of the larger group. While this behavior allows us to quickly absorb and react based on the intelligence of others around us, it also can lead to self-reinforcing cycles of aggregate behavior.

- Overconfidence. We tend to over-estimate our intelligence and capabilities relative to others. Seventy-four percent of professional fund managers in the 2006 study “Behaving Badly”believed they had delivered above-average job performance.

The greater fool theory posits that rational people will buy into valuations that they don’t necessarily believe, as long as they believe there is someone else more foolish who will buy it for an even higher value. The human tendencies described above lead to a fairly predictable outcome: After an innovation is introduced and a market is formed, people believe both that they are among the few who have spotted the trend early, and that they will be smart enough to pull out at the right time.

Ironically, the combination of these traits predictably leads to these four words: “It’s different this time.”

IT’S DIFFERENT THIS TIME

After two massive bubbles in the U.S. in less than a decade, many people question spotting bubbles ahead of time is so difficult. In every bubble, a number of people do correctly identify the bubble. As in the story of the boy who cried wolf, however, the truth is apt to be disbelieved. The problem is that in every market, there are always people claiming that prices are too high. That’s what makes a market. As a result, the cry of “bubble” is far more often proven wrong than right.

Every potential bubble, however, provides an incredibly valuable frame for deepening and debating the role of human psychology in financial markets. Honestly and thoughtfully examining your own behavior through a bubble, and comparing it to the insights provided by behavioral finance, can be one of the most valuable tools an investor has to learning about themselves.

Sunday 21 April 2013

Ubuntu - 'I am because we are"

Yesterday I read Clement Woo's sharing of this article of anthropologist's observations with Kids from an African Tribe. Here is the story...

An anthropologist proposed a game to the kids in an African tribe. He put a basket full of fruit near a tree and told the kids that who ever got there first won the sweet fruits. When he told them to run they all took each others hands and ran together, then sat together enjoying their treats. When he asked them why they had run like that as one could have had all the fruits for himself they said: ''UBUNTU, how can one of us be happy if all the other ones are sad?''

'UBUNTU' in the Xhosa culture means: "I am because we are"

I shared with my colleagues the concepts of property investment as I wanted them to be empowered too. From young to retiring ones, to open their mind to the concept of investment. "I am because we are"

We shall...

An anthropologist proposed a game to the kids in an African tribe. He put a basket full of fruit near a tree and told the kids that who ever got there first won the sweet fruits. When he told them to run they all took each others hands and ran together, then sat together enjoying their treats. When he asked them why they had run like that as one could have had all the fruits for himself they said: ''UBUNTU, how can one of us be happy if all the other ones are sad?''

'UBUNTU' in the Xhosa culture means: "I am because we are"

I shared with my colleagues the concepts of property investment as I wanted them to be empowered too. From young to retiring ones, to open their mind to the concept of investment. "I am because we are"

We shall...

Saturday 20 April 2013

Cost of Borrowing - What do you need to know.

The following information is taken from this website :

http://www.icompareloan.com/resources/home-loans-how-to-compute-the-effective-and-nominal-interest-rates/

—— Eq 1

—— Eq 1

—– Eq 2

—– Eq 2

http://www.icompareloan.com/resources/home-loans-how-to-compute-the-effective-and-nominal-interest-rates/

Home Loans: How To Compute The Effective And Nominal Interest Rates?

Home Loans: How To Compute The Effective And Nominal Interest Rates?

By SUSAN TEO

Interest rate is the cost of borrowing. But the interest rate stated in our credit cards or loans applications may not be the true cost. The rate given is the per annum (p.a.) rate. For example, in a home loan letter of offer you may find a line that says, “First year interest rate is 1% p.a.”. But since the base period for interest calculation (compounding or conversion) can be more than once a year, there can be a difference in interest cost for loans with the same interest rate per annum, loan amount and duration.

The frequency in which the outstanding loan amount is calculated, is also known as rest.

Most Singapore home loans follow a monthly rest, while a few is on daily- and annual-rest basis. All else being equal (including the frequency of instalments), a shorter rest will reduce interest payment.

Thus an effective annual interest rate is needed to measure the true borrowing cost. The interest rate per annum is only the nominal interest rate. This nominal rate is equal to the effective rate when a loan is on annual-rest basis and instalments are also made annually.

In the reminder of this article, I will attempt to teach you how to obtain the annual effective rate and nominal rate, with formulas or Excel, for loans with different frequencies of compounding.

What is the maths formula for the annual effective rate?

—— Eq 1

The annual effective interest rate, re, is actually the ratio of the amount of interest earned during a year to the amount of principal outstanding at the beginning of the year.

The above equation, Eq 1, shows the relation between the effective rate and nominal rate.

So, if you take a monthly-rest loan with an interest rate of 5% p.a., to find the annual effective rate you first define

An important point to note is that the effective rate is always larger than the nominal if compounding is done more than once a year, m > 1.

For a daily compounding loan, the

m = 365, and

m = 365, and

Table 1 presents the effective rate across the three different rests:

Table 1

Type of loan

|

Effective rate (%)

|

| Daily-rest with daily instalments |

5.13

|

| Monthly-rest with monthly instalments |

5.12

|

| Annual-rest with annual instalments |

5.00

|

Please note that the effective interest is lower (reduced interest payment) for shorter rest loans only if the frequency of instalments are the same, and all else are equal. For example, comparing a daily-rest loan with monthly instalments and a monthly-rest loan with monthly instalments, the former will have a lower effective rate.

What is the maths formula for the annual nominal rate?

Conversely, if you have the effective rate, but wish to find the nominal. You can use the below formula:

—– Eq 2

Using the same example, and inserting the values into Eq 2:

we obtain the nominal rate of 5%, as expected.

What are the Excel functions?

Instead of doing the computation with a calculator, you can let Excel do it for you.

Table 2: Maths Formulas and Excel Functions

| Maths Formula | Excel Function |

| | = EFFECT (nominal_rate, npery) |

| | = NOMINAL (effect_rate, npery) |

where npery is equivalent to m, or the number of compounding per year.

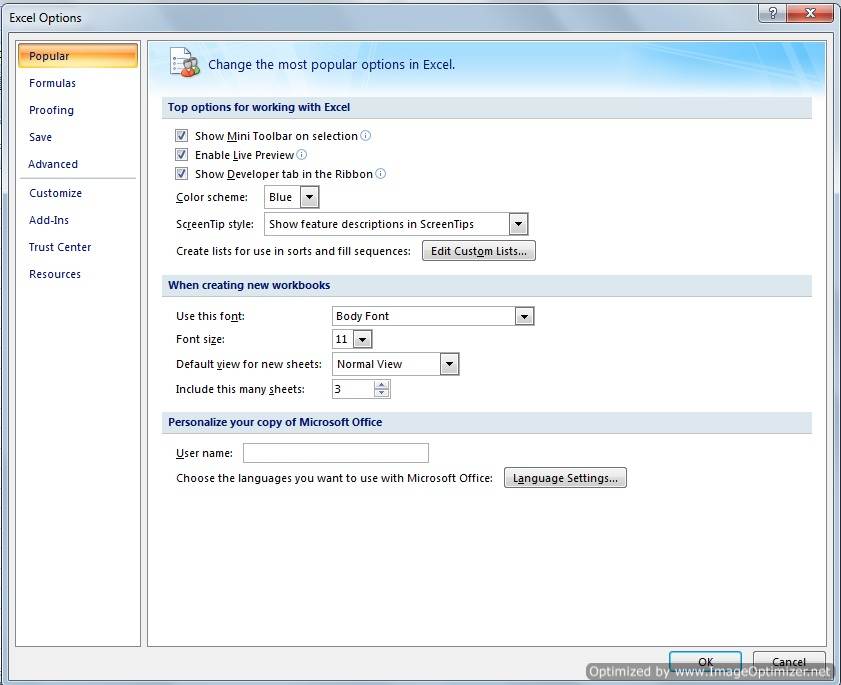

But before you can uitlise these two Excel functions, you need to include an add-on – the Excel Analysis ToolPak. To do so in Excel 2007, you have to click on the Office button on the top left- hand corner as in Figure 1.

Figure 1

Next, you click on Excel Options, and a window will pop up as in Figure 2.

Figure 2

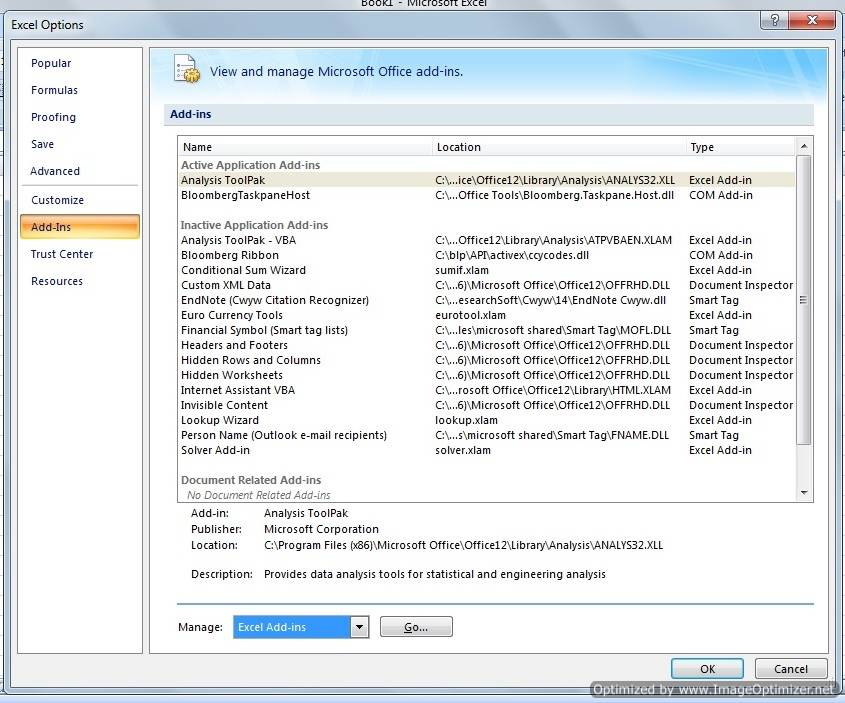

Select Add-Ins, and this will bring you to the next screen:

Figure 3

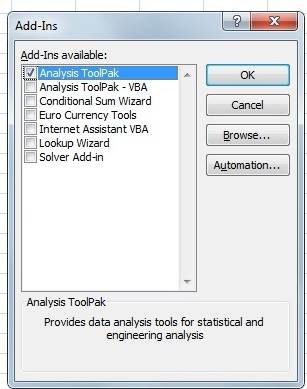

Under “Manage”, make sure “Excel Add-ins” is selected than click Go… The Add-Ins window will appear as seen in Figure 4.

Figure 4

Mark the check-box for “Analysis ToolPak” and click OK. Now you are all set to use the EFFECT and NOMINAL functions.

For advice on a new home loan.

For refinancing advice.

Download this article here.

Melaka - UNESCO World Heritage Site

How do we choose a property?

I learnt from Mr Hubert Ong of MISS that you have to look at the property 300 years from now. How would the unique selling point change? Wow... 300 years... what will really happen?

Many people believe buying in the capital city next to financial district is safe...

Can the capital city move?

Many people choose waterfront location and pay a hand and a leg for it...

Can the shoreline extend?

What cannot change? History? When you are building next to the World Heritage Site, can the World Heritage Site move? 300 years later, it will just be 300 years older and more valuable. This must be the safest bet according the criteria set by Mr Hubert.

This makes Melaka - a UNESCO World Heritage Site and a new hot travel location for the Chinese a worthy look.

Melaka, 3rd smallest state amongst the 13 states of Malaysia and occupying a strategic location between KL and Singapore offers to the visitors a unique heritage of having been colonised and influenced by the Dutch, the Portugese, the British, the Straits Chinese. Some argued that it is from here, the Chinese Empire's influence grew in South East Asia through the visit of Rear Admiral Cheng Ho. Such illustrious history captured in the city's architecture and culture.

After the conferment of the World Heritage Site Status in 2008, the visitor ship grew by double digits each year. Melaka has also transformed itself from a backwater towns full of old buildings to a highly vibrant and dynamic young city as you may call it. There are countless of commercial opportunities brought about by the massive tourist arrivals. There are now ferris wheel ride and look out towers, a live "Jonker" street, a massive shopping complex full of young local people and numerous 4-5 stars hotel sprouting in and around the city centre.

Watch this space as Melaka rise to meet the demands of travellers.

I learnt from Mr Hubert Ong of MISS that you have to look at the property 300 years from now. How would the unique selling point change? Wow... 300 years... what will really happen?

Many people believe buying in the capital city next to financial district is safe...

Can the capital city move?

Many people choose waterfront location and pay a hand and a leg for it...

Can the shoreline extend?

What cannot change? History? When you are building next to the World Heritage Site, can the World Heritage Site move? 300 years later, it will just be 300 years older and more valuable. This must be the safest bet according the criteria set by Mr Hubert.

This makes Melaka - a UNESCO World Heritage Site and a new hot travel location for the Chinese a worthy look.

Melaka, 3rd smallest state amongst the 13 states of Malaysia and occupying a strategic location between KL and Singapore offers to the visitors a unique heritage of having been colonised and influenced by the Dutch, the Portugese, the British, the Straits Chinese. Some argued that it is from here, the Chinese Empire's influence grew in South East Asia through the visit of Rear Admiral Cheng Ho. Such illustrious history captured in the city's architecture and culture.

After the conferment of the World Heritage Site Status in 2008, the visitor ship grew by double digits each year. Melaka has also transformed itself from a backwater towns full of old buildings to a highly vibrant and dynamic young city as you may call it. There are countless of commercial opportunities brought about by the massive tourist arrivals. There are now ferris wheel ride and look out towers, a live "Jonker" street, a massive shopping complex full of young local people and numerous 4-5 stars hotel sprouting in and around the city centre.

Watch this space as Melaka rise to meet the demands of travellers.

Key Ideas towards financial freedom

These are the key ideas which I have learnt and I would like to share it with everyone...

1. Maintain Cashflow positive at all times. Cashflow consists of both income and expenses. It is pertinent that cashflow be maintained at all times. Even with considerable cash savings, with a monthly outflow, the monthly cash outflow will eat into the reserves. Evaluate the deal for cash-flow, if you will experience negative cashflow, the deal is likely not for you at this time. |

||

| 2. Build Passive income - it is forever. Create cash-cows that will build you passive income and property being as iliquid as it is, would create for you passive income. It is these "drops of water" that forms the Ocean. Do not feel the need to hasten your process. The time will come once your passive income builds up... | ||

| 3. Reduction in loan does not increase passive income The difference between active income and passive income is such that passive income works even when you are asleep. So during your growth and expansion phase, there will be decisions to make whether to reduce debts and liabilities with the money saved or to continue to expand. I'll leave it to you to manage that part, however, reducing debts does not mean increasing passive income, it simply means there is an increase in cashflow, however, it also means you still have to work... | ||

| 4. There are good loans and bad loans - Good Loans give you

positive passive income forever 'nuff said. Don't be afraid to take loans. Some will help you to achieve your goals faster. Savings will take you forever if not never to achieve financial freedom. |

||

| 5. Bad loans takes money out of your pocket every month and

should be killed immediately. Bad loans as the name implied is just about taking money out of your pocket. These includes car loans, credit card loans amongst others. |

||

| 6. Create multiple source of income Property is not the only means to earn passive income. EXPLORE! CREATE! Businesses are the real means to great financial success. Be careful though. | ||

7. Risks can be managed with enough research Research, research and research! it is more important to location location location. Make sure you know every single details of the deals. That will allow you to mitigate risks and reap rewards later! | ||

| 8. All deals can be negotiated to your advantage, if not, you are not forced to buy. All deals CAN be negotiated. Negotiate deals yourself and learn! instead of relying on group purchases, you can learn more things and be more independent. Knowledge is the true wealth and doing it will only increase your knowledge. |

||

| 9. Think BIG (from

Donald TRUMP) If you have to negotiate a deal, make it a big one! the amount of time spent negotiating a small deal is the same as one negotiating a big deal. Think BIG! |

Leveraging

What is leveraging? In essence, leveraging is to use a small amount of money to control a large amount of money... As an investor, you need to know your leverage power and as you have already known, your leverage power is a function of your earning power and your credit score amongst others. Always review your credit limit. I just did mine and happy to know I have much greater leverage now and bankers are offering their service to me, instead of me begging them for credit loan! So always review your credit limit every 6 months.

Using Faizul Rizuan's example, each credit card would be able to leverage up to 4 x your monthly salary and allows you (if your credit score is good) interest free loan and / or low interest balance transfer.

Using this method, it would be easy to raise a sizable amount of money for down payment fairly quickly. The more you earn, the more you can leverage.

A guide would be about $500 / month for 4 years for about $20,000 for 1 bank.

Always remember even with the above mentioned method, it is prudent to have positive cashflow at all times!

Using Faizul Rizuan's example, each credit card would be able to leverage up to 4 x your monthly salary and allows you (if your credit score is good) interest free loan and / or low interest balance transfer.

Using this method, it would be easy to raise a sizable amount of money for down payment fairly quickly. The more you earn, the more you can leverage.

A guide would be about $500 / month for 4 years for about $20,000 for 1 bank.

Always remember even with the above mentioned method, it is prudent to have positive cashflow at all times!

Cashflow - the key to financial freedom

Cashflow. I have just recently completed cashflow 202 game, it is an important milestone for me. I used to be trashed at cashflow 101 and really did not know how to get out of the rat race. Over the 3 years of educating myself through talks and discussions.

Over the last 3 years, I have accumulated 6 properties using as little money down as possible and having tenants which pays for my mortgage.

Property A - $1000

Property B - ($120) - 90% mortgage

Property C - $270

Asset D - $400

Property E - $500

Property F - $500

I'm very proud to say I'm halfway to being financially free! All holding down a full time job. In fact Asset D, property E and F are assets which are bought within 2013. I believe the path ahead will be an upward projectory.

Please read Robert Kiyosaki, Faizul Ridzuan, Marco Robinsons' books and please please attend all the free talks there is out there and ask questions... learn from the masters. You need to keep abreast of everything that is happening even as you do not have the cash to invest for you may learn how to unlock your potential in you.

Subscribe to:

Posts (Atom)